Market dynamics remain unchanged

Scott Sanchon, Trade Treasury Payments

Open account trade accounts for 80% of global trade, but managing payment risk and cross-border transactions has never been more complex. Financial institutions are now seeking frameworks that offer predictability and legal clarity.

In May 2026, FCI, the global representative body for factoring and financing of open account domestic and international trade receivables, published an executive brief explaining how its cross-border trade finance framework works and ultimately addresses challenges in the current economic uncertainty.

Market dynamics remain unchanged

In practice, cross-border factoring, corporates and SMEs sell or assign their unpaid receivables to a factoring company, converting outstanding invoices into working capital while transferring the credit risk of non-payment to the factor.

FCI’s core legal framework, the General Rules for International Factoring (GRIF), governs the assignment and collection of accounts receivable between FCI member institutions and continues to apply as normal. This legal framework sets out the rules on systems, procedures, and arbitration that reinforce cross-border factoring transactions in good faith.

As geopolitical disruption and trade volatility increase in prevalence, supply chain disruption, counterparty uncertainty, and shifting trade corridors create significant challenges for businesses. FCI’s framework, however, is designed to address those pressures without requiring changes to the rules and regulations.

The two-factor model and why it matters

At the heart of FCI’s cross-border solution is the two-factor model, where the export factor and the import factor each operate in their respective regional markets. This model is a structure that distributes responsibility and credit risk between two financial institutions.

Under the model, the export factor purchases accounts receivable from an exporting supplier under an executed factoring agreement. Those receivables are owned by a debtor located in the importing factor’s country. The two factors will negotiate the commission to be paid to the import factor, the level of credit coverage, and the terms of credit approval for the transaction. If the importer agrees to purchase the accounts receivable, it assumes the credit risk of non-payment up to the approved coverage amount.

This practice is what makes FCI’s model extremely effective for cross-border trade. The export factor has direct knowledge of the supplier, while the import factor has direct knowledge of the debtor. These two factors create a structure in which both sides are covered by institutions with local market expertise, while offering a level of risk management that open-account trade cannot.

The scale of adoption reflects this confidence, with cross-border factoring volumes reaching close to €4 trillion in 2025 at a 20-year CAGR of 7.1% according to FCI’s May 2026 executive brief.

What if a debtor cannot pay?

Under the two-factor model, the import factor’s assumption of credit risk provides exporters with protection against credit risk.

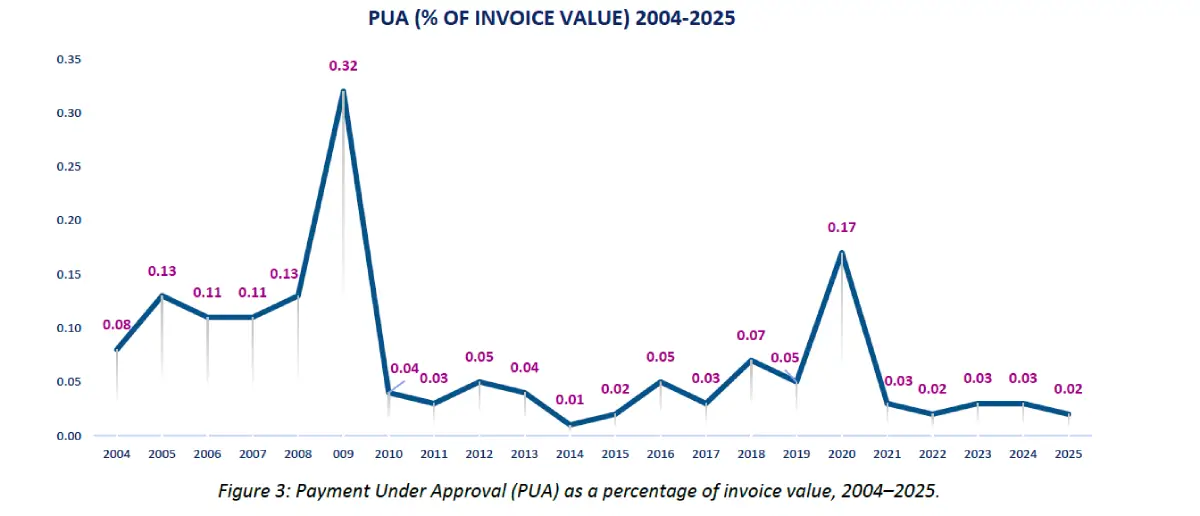

Payment Under Approval (PUA) is a key mechanism. If an approved account receivable stays unpaid for ninety days, the importer is required to immediately pay the export factor the full purchase price of that receivable on that date.

This structure helps exporters build strong confidence in the payments of approved receivables, regardless of debtors’ circumstances.

FCI’s data from 2004 to 2025 shows that the PUA percentage of invoice value has remained consistently low, peaking at 0.32% during the 2008 financial crisis and trending around 0.03% in recent years. This ensures clients benefit from timely payments, even when debtors delay or default.

Managing commercial disputes

Under GRIF, the term ‘dispute’ covers any reason claimed by a debtor for non-payment, including defences, counterclaims, or set-off claims raised by a debtor.

When a dispute arises, the importer’s credit risk assumption is suspended. The export factor is responsible for resolving the dispute and must act continuously to resolve it as soon as possible. Moreover, the import factor may provide its services to assist in resolving the dispute, whether through negotiation or legal action. If the dispute is settled in favour of the supplier, the import factor’s credit coverage is reinstated, and PUA will be made. If the dispute is resolved in favour of the debtor, the importer’s liability on that receivable is eliminated.

These structured processes help ensure that credit and commercial risks stay separate. It is particularly valuable when the economic uncertainty and trade disruptions make payment less predictable.

Alignment challenges across FCI members

In the rare event that the import factor and the export factor disagree over the application of the GRIF, the framework requires both parties to submit to final and binding arbitration conducted by FCI. Arbitrators are drawn from a panel of factoring experts, and FCI’s Rules of Arbitration govern the procedure.

In nearly six decades, only eight formal arbitrations have been held, a figure that speaks to the network’s collaborative culture and the clarity of the GRIF.

Strategic implications for business

FCI’s cross-border framework was built to address the uncertainty that characterises the current global trade environment. The GRIF continues to provide the legal enforceability and operating efficiency needed to trade confidently across borders.

In the meantime, FCI recommends that members continue applying the GRIF in the usual manner and maintain communication with counterparties on transactions.

Article Info

Related Articles

Central Bank Digital Currencies (CBDCs) +4

Central Bank Digital Currencies (CBDCs) +4Why digital money’s real test is governance

By: Lewis Sun, Global Head of Digital Currencies, Corporate and Institutional Banking, HSBC. For years,...

Development Finance +3

Development Finance +3Bridging the trade finance gap: How blended finance is reshaping trade and development

By: James Dorman, Trade Treasury Payments (TTP) Trade is perhaps the most powerful engine for...

Cross-Border Payments +4

Cross-Border Payments +4Last orders: Europe prepares to put FX markup on the label

By: Tim Staheli, Writer & Editor, Trade Treasury Payments At a fintech summit in London...

Stay Ahead of the Curve

Get exclusive insights, expert analysis, and breaking news on liquidity and risk management, delivered to your inbox

Article Info

Stay Updated

Get the latest insights on trade finance, treasury management, and global payments delivered to your inbox.

Join 25,000+ professionals. Unsubscribe anytime.